Canadian savers who think that their money is safe sitting in their bank accounts earning a supposedly low risk return of less than 1% are effectively having their wealth stolen by those same banks through inflation rates that are running much higher than this.

But that’s not all!

The Canadian federal government has introduced their little publicized “bank bail-in regime” in the 2016 budget last year.

“Introducing a Bank Recapitalization “Bail-in” Regime

To protect Canadian taxpayers in the unlikely event of a large bank failure, the Government is proposing to implement a bail-in regime that would reinforce that bank shareholders and creditors are responsible for the bank’s risks—not taxpayers. This would allow authorities to convert eligible long-term debt of a failing systemically important bank into common shares to recapitalize the bank and allow it to remain open and operating. Such a measure is in line with international efforts to address the potential risks to the financial system and broader economy of institutions perceived as “too-big-to-fail”.” Source

When you deposit money into your bank savings account, you in effect are lending money to the bank. In effect, you become a “creditor” to the bank since the bank now owes you that money you deposited and is paying you interest, as pathetically low as it may be right now, on the money you lent to the bank.

The “Bail-In” regime indicates that: “…bank shareholders and creditors are responsible for the banks risks – not the taxpayers.” Well guess what, even though you may be a taxpayer, the reality is that if you have a deposit at that bank or if you decided to follow the “common wisdom” financial advisor advice by investing in the supposedly “Blue Chip” dividend paying bank stocks, thereby making you a shareholder, then you are on the hook!

“Taxpayer” really means “the Federal Government” which derives the vast majority of their revenues from taxpayers, hence the term used.

What this means is that if a Canadian bank starts to fail, it would be allowed to seize the money in your bank account or wipe out your shareholder value if you happen to own that bank’s stocks to pay its bills. Really!

Forget about the likes of Bernie Madoff, the Feds have made this new type of theft legal.

Is it not time that Canadians learn the truth about the true nature of our fiat currency, the dollar?

“Fiat money is currency that a government has declared to be legal tender, but it is not backed by a physical commodity. The value of fiat money is derived from the relationship between supply and demand rather than the value of the material that the money is made of.” Source:

What this means is that the value of our money is based solely on what it is perceived to be valued and the amount of those bills and coins in circulation.

You may have noticed that the goods and services you buy today are getting more and more expensive each and every year. So you may conclude that the value of those same goods and services continue going up, but you would be wrong!

The reality is that it is not the prices that is moving up, rather it is the value of our currency, the Canadian dollar that is actually going down annually.

The more money our government prints, the more supply of money in our system, the more our money continues to go DOWN in value and therefore the less our money can buy tomorrow than it can today.

So let’s put this into terms everyone can relate to.

How Much Are Your Eggs Worth In Your Basket?

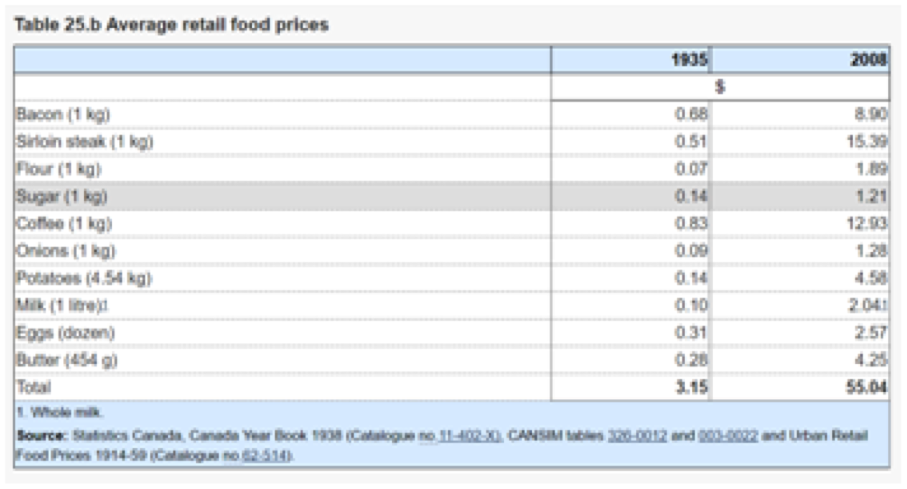

The above chart (compliments of Stats Canada) indicates average retail food prices over a 73 year period from 1935 to 2008. In 1935, you could have purchased all of the items listed for only $3.15 yet in 2008 you would need $55.04 to buy those very same items. That right, in 2008 it would take 17.5 X the amount of money in it would take to buy those very same groceries in 1935.

So naturally, you may assume that the prices of these groceries have gone up by 1,747% and you would be wrong!

You see, the grocery items indicated in the chart have not increased in value at all. Rather it is the value of our Canadian dollars that have eroded in value by 1,747%.

The truth is that it is not prices for goods and services going up each and every year. Instead it is the purchasing power of those dollars that are going down in value.

Don’t believe me? Say you were to stuff a $100 dollar bill stuffed under your mattress back in 1935, what would it be worth today? Surprise, that $100 piece of paper would still be $100 dollars today. The only difference is the amount of purchasing power that $100 has today vs. what it had in 1935.

In fact, in 1935 you could buy with $100 what it would take you $1,801.73 today, in 2017, to buy with those very same dollars. This means that it would now take over 18 times the amount of money to buy those very same goods and services! Source

Now let’s assume that those same basket of groceries were none perishable hard assets. An egg from 1935 would still be an egg in 2017 and it would retain and hold the exact same value today as it would have in 1935.

Now instead lets use a true non-perishable hard asset like a house in Toronto.

Back in 1935, the average cost of new house in Toronto was $3,450 and the average wages per year were $1,600 per year. Source:

Today the average price for a detached home in Toronto was $1,336,640. Source: TREB

This means that it now would take more than 387 X the amount of dollars to buy that very same property today, a staggering 38,743% more!

Now, that would all be fine and dandy, except for one very big, BIG wrinkle.

As indicated above, in 1935 the average wage in Toronto was $1,600 per year. Yet by 2016, the average salary in Ontario only rose to $50,589 or by slightly less than 32 X the amount of dollars it would take to earn those same wages in 1935. Yet the value of your labour, your work should technically remain the same.

Average wages have gone up 32 X in dollars since 1935, yet the average detached home prices have gone up 387 X over the same period. So home prices have risen 12 X more and faster than average wages.

Is it any wonder why houses in Toronto seem so ridiculously less affordable than ever? That’s because they truly are less affordable.

How To Get Poor By Saving More

Incredibly, even in light of this stark truth our schools and universities continue to propagate bogus financial education and telling us to “save more”!

This simply makes no sense whatsoever! We have all been taught about building wealth by saving our money our entire lives. Can you see how absurd that is now?

Contrary to what you may hear in the news and media, contrary to what you have been taught all your life by your bank’s financial advisers or teachers in school, who have incidentally been drinking the same “Kool-Aid” and simply don’t know any better themselves, and contrary to all the accepted “common wisdom” we should not be saving more.

After the financial crises of 2007 we now know that the governments have no issues bailing out banks. We also know that the feds are now prepared to allow those same banks to keep your cash should they experience similar financial disasters in the future by allowing them to “Bail-In” your saving held in your savings accounts.

Let’s hope everyone has a big mattress to keep their cash under!

How to Spend Your Way to Financial Freedom:

Instead of saving more we should actually be spending more. Yes, you read that right!

The reality is that we should not be saving any more cash than what is required to sustain our living expense for the short term, say 6-12 months, as an emergency fund. After all, you now know that those dollars you have worked so hard to earn are losing their buying power, that is what and how much they can buy, each and every single day as time goes on.

However, you should not be spending for the sake of spending and no, this does not mean you should run out immediately and book that world wide, year long dream vacation on your credit card just yet (although you can certainly do this and so much more when you achieve your goal of financial freedom).

It may surprise to learn that unlike our North American culture, wealth in the vast majority of countries around the world is not measured by the amount of money someone has in their bank account.

Instead wealth in those countries has been historically been measured by the amount of hard asset they own and more specifically how much income those assets generate to those who own them.

If it’s one thing that all the above numbers and analysis tell us is that if you truly wish to build and retain your wealth you absolutely must spend your money instead of saving it.

Is it not time for an overhaul of our financial education system?

Should we not be focused on educating our children, and all Canadians for that matter, on how to spend your money to invest in hard assets?

Specifically, should we not be protecting our hard earned money by spending it to buy hard assets like gold, silver and other precious metals to protect the value of our hard earned dollars? Dollars, whose value we now know will continue to depreciate in value as time goes on.

Better still, we can spend our money to buy self paying hard assets that generate positive cash flow, today, tomorrow and quite possibly forever, like cash flow positive investment properties? Remember:

“Without Money Working for You, You Will Always Be Working for Money!”

Of course you can choose to continue following the “common wisdom” by saving more your hard earned money.

But ask yourself, how has that been working for you?

Are you any closer to achieving your financial goals or your financial freedom?

Let’s just hope and pray that high inflation does not rear it’s ugly head anytime soon. Because if (and I personally believe it is a matter of when, not if as history tends to repeat itself) that happens all those savers could very well be forced to kiss their hard earned savings in their bank accounts goodbye and with that any hopes and dreams of financial freedom they may have had.

Is it not time to protect your “Ass”ets?